The One-Two Punch American Households Didn’t Need

First came the bad news. Then came worse news.

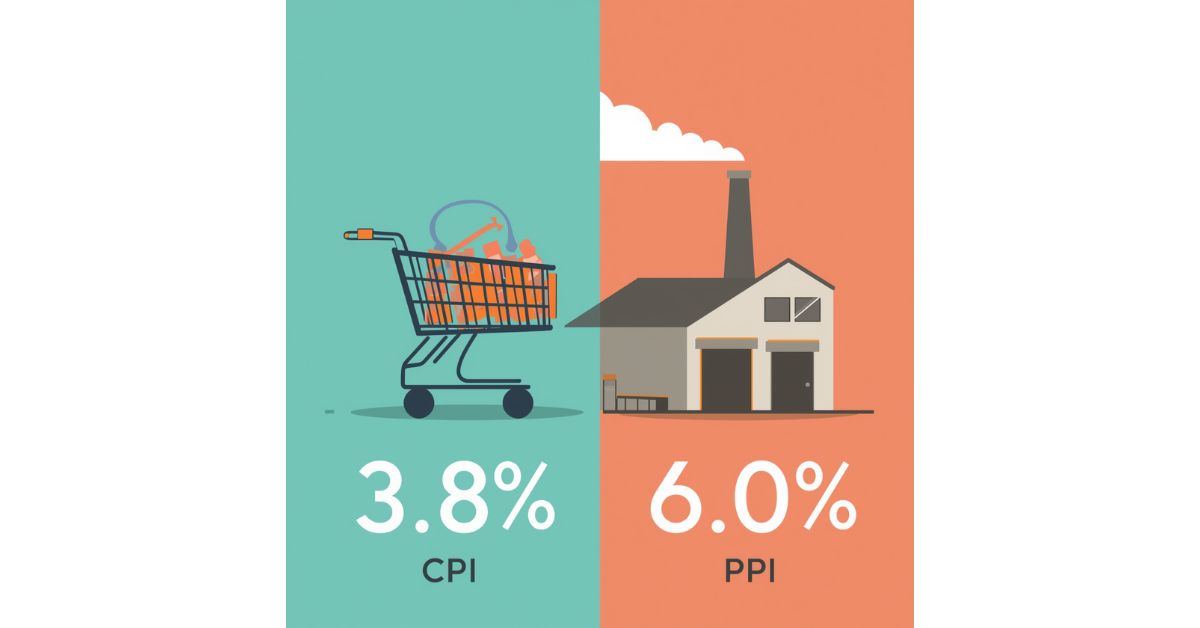

On Tuesday, the Bureau of Labor Statistics dropped the April Consumer Price Index (CPI) — the government’s monthly snapshot of what Americans pay for everyday goods. The number: 3.8% year-over-year, the highest since September 2023 .

On Wednesday, the BLS followed up with the April Producer Price Index (PPI) — which measures what businesses pay for raw materials, supplies, and wholesale goods. That number was even worse: 6.0% year-over-year, the highest since December 2022 .

Together, these two reports paint a troubling picture: Inflation is accelerating at every level of the economy — from the factory floor to the grocery store checkout line.

For American households, here is what this double inflation shock means right now — and what you can do about it.

The Numbers: What You Need to Know

CPI (Consumer Prices) — What You Pay

| Category | April 2026 Reading | March 2026 Reading | Why It Matters to You |

|---|---|---|---|

| Headline CPI | 3.8% (YoY) | 3.3% | Highest since Sept 2023 |

| Monthly CPI | 0.6% | 0.9% | Still rising fast |

| Energy | +3.8% (monthly) | +10.9% (monthly) | Gas, electricity, heating oil |

| Gasoline | +5.4% (monthly) | +21.2% (monthly) | $4.50+ per gallon |

| Food at home | +0.7% (monthly) | -0.2% (monthly) | Grocery bills are back up |

| Meats, poultry, fish, eggs | +1.3% (monthly) | — | Beef up 2.7% in one month |

| Fruits & vegetables | +1.8% (monthly) | — | Fresh produce spiking |

| Shelter | +0.6% (monthly) | +0.3% (monthly) | Rent and housing costs rising faster |

Source: U.S. Bureau of Labor Statistics, April 2026 CPI Report

PPI (Wholesale Prices) — What Businesses Pay (Before You Pay)

| Category | April 2026 Reading | Forecast | Why It Means Higher Prices for You |

|---|---|---|---|

| Headline PPI (YoY) | 6.0% | 4.9% | Highest since Dec 2022 |

| Monthly PPI | 1.4% | 0.5% | Triple the forecast |

| Core PPI (YoY) | 5.2% | 4.3% | Inflation spreading beyond energy |

| Monthly Core PPI | 1.0% | 0.4% | Double the forecast |

| Wholesale energy | +7.8% (monthly) | — | Producers paying more for fuel |

| Wholesale gasoline | +15.6% (monthly) | — | Will hit pump prices soon |

Source: U.S. Bureau of Labor Statistics, April 2026 PPI Report

Why the PPI Number Matters More Than You Think

Many personal finance websites focus only on CPI. That is a mistake.

PPI is a leading indicator. What producers pay today, you pay tomorrow — usually 1 to 3 months later .

Here is the pipeline of pain:

April 2026 PPI: 6.0%

↓

(1-3 months)

↓

Future CPI: Expected to rise further

↓

Your wallet: Higher prices for everything

Over 40% of April’s wholesale price surge came from gasoline alone, which jumped 15.6% . But the increases are spreading beyond energy — core PPI (excluding food and energy) hit 5.2%, its highest level since December 2022 .

This means the inflation you are feeling right now is not “transitory.” It is the new normal — at least for the rest of 2026.

What This Means for Your Wallet — Right Now

Your Grocery Bill (Already Hurting, About to Get Worse)

The April CPI already showed painful increases at the supermarket:

| Grocery Item | April Increase | Annual Increase |

|---|---|---|

| Beef | +2.7% (one month!) | — |

| Fruits & vegetables | +1.8% (one month!) | +6.1% (year) |

| Nonalcoholic beverages | +1.1% (monthly) | +5.1% (year) |

| Eggs & poultry | +1.3% (monthly) | — |

| Food at home (overall) | +0.7% (monthly) | +2.9% (year) |

What to do now:

- Stock up on non-perishables when on sale. Prices are not coming down.

- Consider bulk buying with family or neighbors to split costs.

- Look for store brands — name brands will raise prices first.

Your Gas Tank and Utility Bills

Energy prices are the primary driver of both CPI and PPI inflation .

| Energy Item | April Increase | Annual Increase |

|---|---|---|

| Gasoline | +5.4% (monthly) | +28.4% (year) |

| Fuel oil | +5.8% (monthly) | +54.3% (year) |

| Electricity | +2.1% (monthly) | +6.1% (year) |

What to do now:

- Combine trips to reduce driving.

- Check with your utility about budget billing (spreads costs evenly across the year).

- Look into energy-efficient appliances — the upfront cost may pay off faster than expected.

Your Mortgage and Rent

The shelter index (rent and homeownership costs) rose 0.6% in April — double March’s 0.3% increase . This is a critical number because shelter makes up a huge portion of most household budgets.

What to do now:

- If you are renting and your lease is up for renewal, expect a 3-5% increase — budget accordingly.

- If you are buying a home, do not wait for lower mortgage rates. Bank of America now expects no rate cuts until 2027 .

Your Savings Account (The One Bright Spot)

Higher inflation means the Fed will keep interest rates high. That is bad for borrowers but good for savers.

High-yield savings accounts (HYSAs) are still offering 3.5% to 3.7% APY at top online banks.

What to do now:

- Lock in a 12-24 month CD at 4.0% to 4.5% if you have cash you will not need soon.

- Keep your emergency fund in a HYSA — do not leave cash earning 0.01% at a traditional bank.

The Fed’s Dilemma: No Rate Cuts in 2026

The double inflation shock has fundamentally changed the Federal Reserve’s outlook.

| Bank | Previous Rate Cut Forecast | New Forecast |

|---|---|---|

| Bank of America | One cut in late 2026 | No cuts until 2027 |

| Goldman Sachs | First cut Sept 2026 | First cut Dec 2026 or later |

| Market pricing (CME FedWatch) | Cuts expected mid-2026 | 62% chance of zero cuts in 2026 |

Source: BofA Global Research, Goldman Sachs, CME FedWatch Tool

The Fed’s April meeting was already unusually divided — an 8-4 vote, the closest since 1992 . Now, with inflation accelerating, the chance of rate cuts in 2026 has effectively died.

In fact, prediction markets now show a 39% probability of a rate hike before the end of 2026 .

What Economists Are Saying

Aditya Bhave, Bank of America (head of U.S. economics):

“The data simply don’t warrant cuts this year. Core inflation is too high, and moving up. The solid April jobs report was the last straw, especially given hawkish Fedspeak.”

Bank of America research note:

“We think incoming Fed Chair Warsh will push for lower rates, but the data flow precludes cuts for now. However, cuts should be in play by next summer, with inflation much closer to target.”

The Wall Street Journal (citing economists):

“Economists polled by The Wall Street Journal were expecting a 0.5% rise (in PPI). The actual 1.4% increase blew past expectations.”

Old North State Wealth Management:

“Today’s 6% PPI report killed any realistic chance of Fed rate cuts in 2026.”

What You Should Do This Week (Not Next Month)

If You Have Credit Card Debt

This is the most urgent action item. Waiting for rate cuts that are not coming has already cost you money.

| Debt Amount | APR | Interest Paid Waiting 12 Months |

|---|---|---|

| $10,000 | 24% | ~$2,400 |

| $15,000 | 24% | ~$3,600 |

| $25,000 | 24% | ~$6,000 |

Source: Old North State Wealth Management analysis

Your options right now (no Fed approval needed):

- 0% balance transfer cards — Still available for credit scores of 670+ with 15-21 month promotional periods .

- Call your card issuer’s hardship department — Every major bank has one. Request a rate reduction (often to 6-12%) .

- Consider a debt management plan or bankruptcy consultation — Not a last resort, a math-based decision. Bankruptcy has a 95% discharge rate and protects retirement accounts .

If You Are Saving or Investing

| Goal | Action |

|---|---|

| Emergency fund | Keep in HYSA (3.5-3.7% APY) |

| Cash not needed for 12-24 months | Lock in a CD at 4.0-4.5% |

| Stock investments | Reduce tech exposure (rate-sensitive). Add energy (benefiting from oil >$100) and financials (banks earn more with high rates). |

| Retirement contributions | Do not stop. Compound interest works for you, not against you — but only if you stay in the market. |

If You Are Buying a Home

Do not wait for lower rates. They are not coming in 2026. The 30-year fixed mortgage is already near 7.2%. If the Fed actually raises rates, mortgages could climb toward 8%.

Action: Focus on affordability at today’s rates. Consider an adjustable-rate mortgage (ARM) if you plan to move or refinance within 5-7 years — ARMs typically offer lower initial rates than fixed mortgages.

The Bottom Line

The April 2026 inflation data is not a one-month anomaly. CPI at 3.8% and PPI at 6.0% represent a clear trend: inflation is accelerating at every level of the U.S. economy.

The Federal Reserve will not cut rates in 2026. Bank of America, Goldman Sachs, and the CME FedWatch Tool all agree on this now . The only remaining question is whether the Fed will be forced to raise rates again.

For American households, this means:

- Borrowing will remain expensive — Credit cards, mortgages, and auto loans will not get cheaper in 2026.

- Prices at the grocery store and gas pump will stay high — And may rise further as wholesale inflation filters through.

- Savings rates will remain attractive — HYSA and CD rates are worth locking in now.

- Waiting is the most expensive strategy — Especially if you have credit card debt.

The Fed is not coming to rescue you. The tools to protect your finances already exist — a balance transfer, a hardship call, a CD ladder, a diversified portfolio. Use them now.

Check back tomorrow for our analysis of how the April inflation data is affecting the 2026 housing market — and whether home prices are finally starting to cool.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, investment advice, or tax advice. You should consult with a qualified U.S. financial advisor or tax professional before making any financial decisions. Past performance does not guarantee future results.